NIO's about-face highlights the plight now facing China's EV makers, as they try to navigate an unexpected turn in the road that analysts say could stretch on for some time to come.

This article by Trevor Mo was first published in The Bamboo Works, which provides news on Chinese companies listed in Hong Kong and the United States, with a strong focus on mid-cap and also pre-IPO companies.

(Image credit: CnEVPost)

Key Takeaways:

NIO cut its prices last week, reversing its previous position, in response to slowing sales growth over the past two months after many of its rivals made similar reductions.

Smaller firms could be the most vulnerable if the current EV price war drags on, due to their thinner margins compared to larger peers.

Used to being praised for its cutting-edge electric vehicles (EVs), NIO Inc. (NIO.US; 9866.HK) found itself in unfamiliar terrain last week when it became the target of online sarcasm after announcing it would slash prices for all of its electric vehicles (EVs) by 30,000 yuan ($4,209).

Just two months earlier, CEO William Li had proclaimed he would never join the price war now throttling his sector, saying such blind cuts would only lead to "unhealthy competition".

NIO's about-face highlights the plight now facing China's EV makers, as they try to navigate an unexpected turn in the road that analysts say could stretch on for some time to come. Smaller firms are in the most difficult bind since further cuts will further erode their already thin margins. But refusing to stay in the cutting game risks losing sales to industry heavyweights such as BYD (1211.HK; 002594.SZ) and Tesla (TSLA.US).

We'll look shortly at how the recent price war is affecting China's smaller homegrown EV makers, which also include Li Auto (LI.US; 2015.HK), Leapmotor (9863.HK) and XPeng (XPEV.US; 9868.HK), as well as non-listed peers like WM Motor. But first, we'll shift into reverse to see how the ongoing months-long price war has evolved.

Things began last October when Tesla cut prices for its Model 3 and Model Y by as much as 9 percent, then further slashed prices as much as another 13.5 percent in January.

Those cuts prompted others to follow suit, with XPeng announcing reductions in January for its G3i SUV and P5 and P7 sedans by as much as 13 percent. BYD joined the following month by cutting the price of its 2021 Han EV model by 20,000 yuan in Beijing, and the 2021 Qin EV by 15,000 yuan.

Other brands, from domestic heavyweights like GAIC, SAIC, and FAW, to foreign names like Ford, Volkswagen, BMW, and Toyota, also joined the bloodbath. The cuts followed Beijing's retirement of one of the main government incentive programs for EV purchases at the end of last year, which previously helped to double the sector's sales in 2022.

The price war later spilled into the fossil fuel vehicle sector as well, with automakers rushing to clear inventory before a new set of stringent emissions standards takes effect in July.

As of late March, more than 40 carmakers had gotten sucked into the Chinese price war by offering discounts on electric and gas-powered vehicles, according to local media outlet Yicai, which cited data from third-party consultancy Positioning Pioneers.

As the cutting gained traction, about 20 percent of passenger cars being sold in China came with discounts of 10,000 yuan or more, according to PingWest, another local news outlet, citing data compiled by research group China Auto Market.

Driving consolidation

The price war is already showing signs of driving consolidation in a crowded sector whose growth was fueled in no small part by strong government incentives that are now being rapidly phased out.

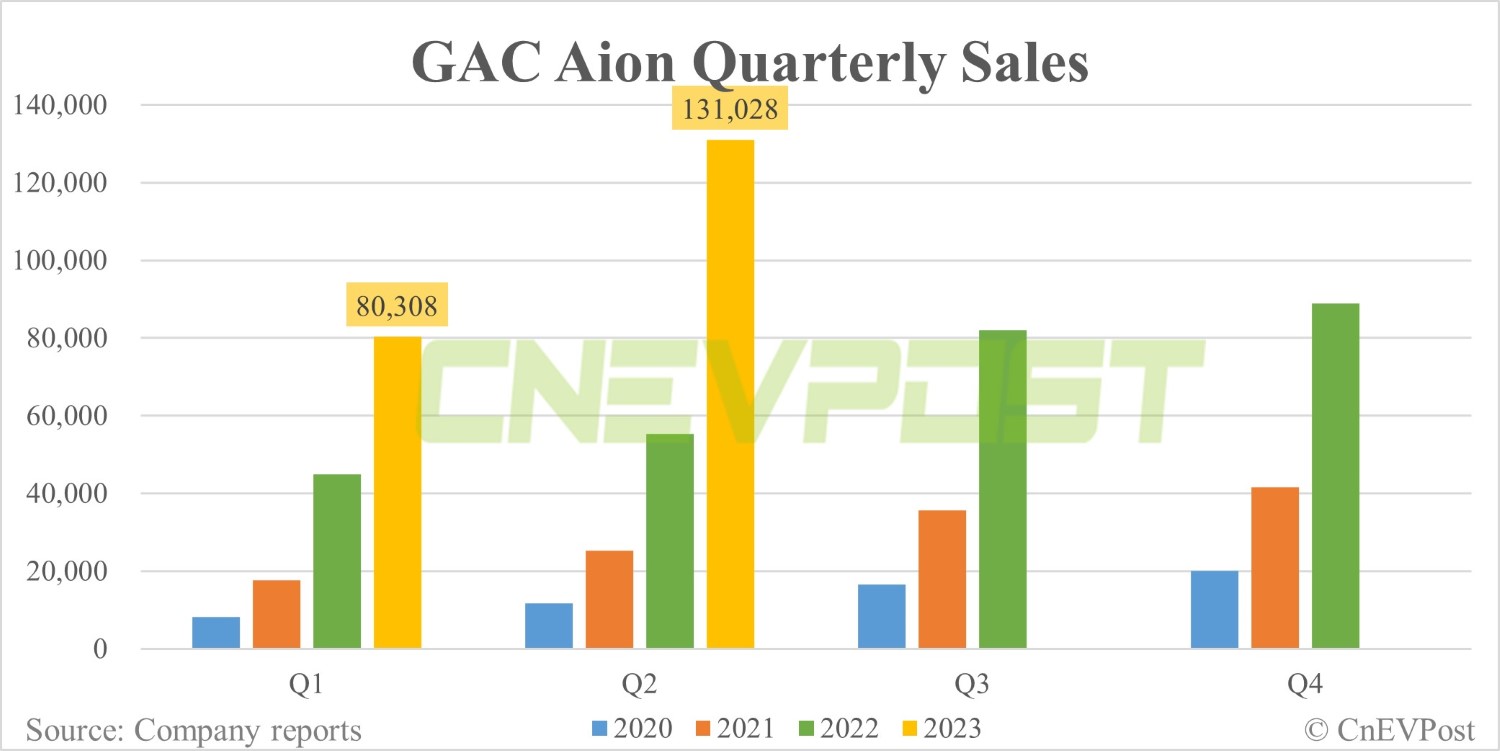

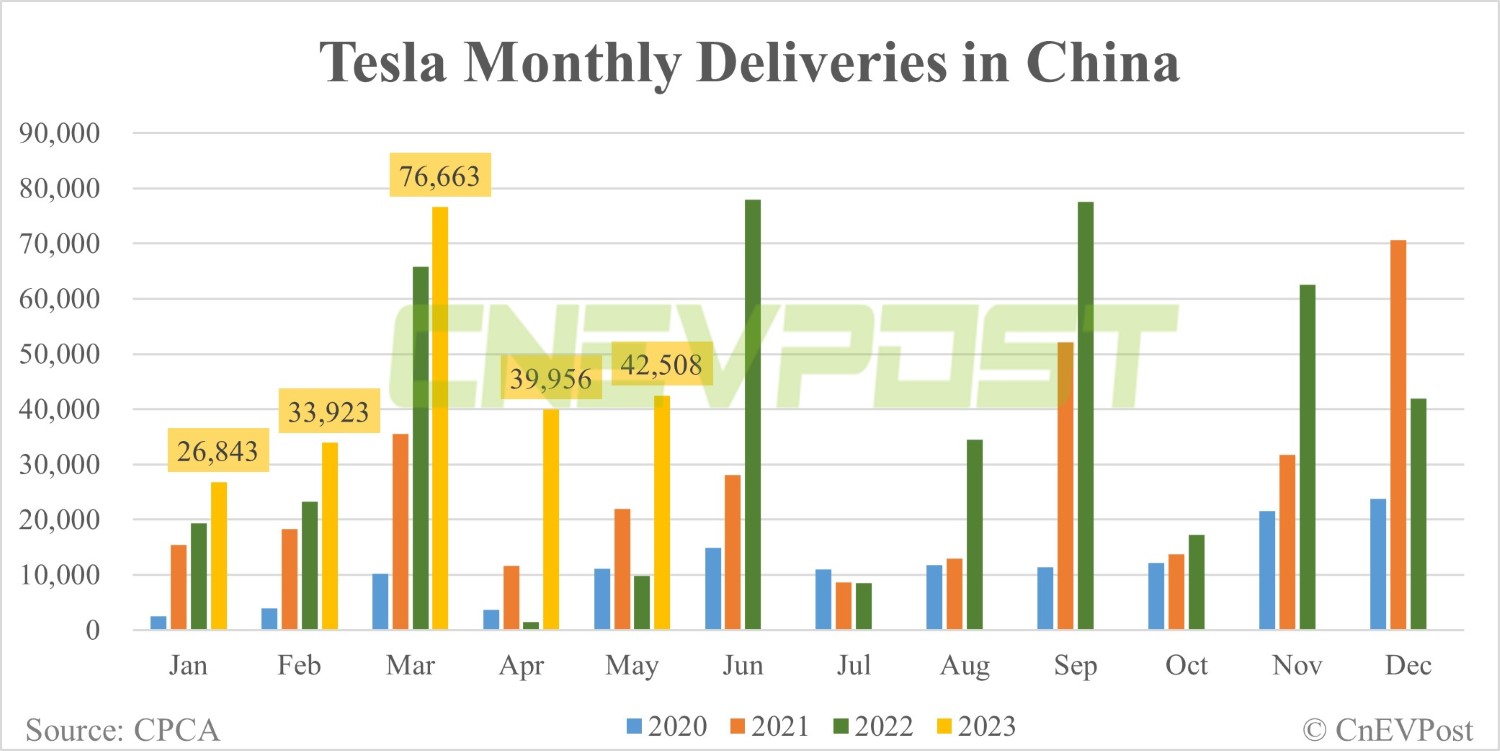

As the war drags on, bigger players are increasingly cementing their leading positions, while smaller ones face sluggish sales. In the first four months of this year, three companies – BYD, Tesla and GAC Aion – held a combined 50.1 percent share of the pure-battery EV market, up from 42.7 percent in the same period a year ago, according to the China Passenger Car Association (CPCA). BYD led the trio with 24.9 percent of the market, up 7.4 percentage points year-on-year.

As the big names gained share, many smaller brands moved in the opposite direction. XPeng reflected that group, symbolically dropping off the list of the top 10 EV makers in the first four months of this year.

NIO managed to increase its share by 0.3 percentage points, but its 27.1 percent growth rate in vehicle deliveries during the period was far behind BYD and Tesla, which each recorded more than 60 percent year-on-year growth.

Facing such slowing growth, it comes as little surprise that NIO has finally joined the price war. But it also remains to be seen whether the move will significantly boost its sales.

XPeng's experience suggests otherwise. Its massive price cuts in January failed to lift sales, and the company's total vehicle deliveries actually plunged by 47.3 percent in the first three months of this year.

Another smaller EV startup, Leapmotor, announced similarly dismal results after rolling out its own massive price cuts. The company's vehicle deliveries tumbled by 51.3 percent in the first quarter to 10,509, according to its latest quarterly report.

Not all smaller players have suffered. Li Auto – the last holdout in the intensifying price war – delivered 52,584 vehicles during the first quarter, up 65.8 percent year-on-year. The company also recorded a 933.8 million yuan net profit for the period, making it one of the few EV makers that has been able to operate profitably. Both BYD and Tesla recorded profits during the period, while NIO, XPeng, and Leapmotor all lost money.

The smaller companies' dismal bottom-line performance is reflected in their profit margins that sharply trail their larger peers. NIO, XPeng, and Leapmotor all recorded gross profit margins of less than 2 percent during the first quarter, well behind BYD's 17.9 percent and Tesla's even higher 19.3 percent for its EV business.

That brings us back to the dilemma now confronting smaller firms that will find it increasingly difficult to wage a prolonged price war that sucks up their dwindling cash hordes, with skeptical investors unlikely to provide fresh funds.

NIO's cash fell to 37.8 billion yuan by the end of March from 45.5 billion three months earlier, while XPeng's fell to 34 billion yuan from 38 billion yuan over the same period. Those declines are likely to continue, or even accelerate if the price war continues.

The war has already left a number of the smallest major EV makers teetering on the brink of insolvency. One of those is WM Motor, a former highflyer that is currently facing a financial crunch that saw it reportedly slash salaries and implement mass layoffs late last year and into 2023. Data from the CPCA showed that WM Motor sold just 457 vehicles in the first two months of 2023, down 92.4 percent from the year-ago period.

BREAKING: NIO cuts starting prices by $4,200 for all models and makes battery swap benefits optional

The post China's EV sector at crossroads as NIO joins bloody price war appeared first on CnEVPost.

For more articles, please visit CnEVPost.